Runtime Governance Series

AI Compliance Frameworks for Financial Services in 2026: Mapping the Territory

What banks, asset managers, and insurers actually need to satisfy regulators across overlapping AI regimes, without halting deployment

Published on

AI compliance in financial services in 2026 is not constrained by the number of frameworks. It is constrained by whether institutions can produce verifiable evidence of AI behaviour at runtime.

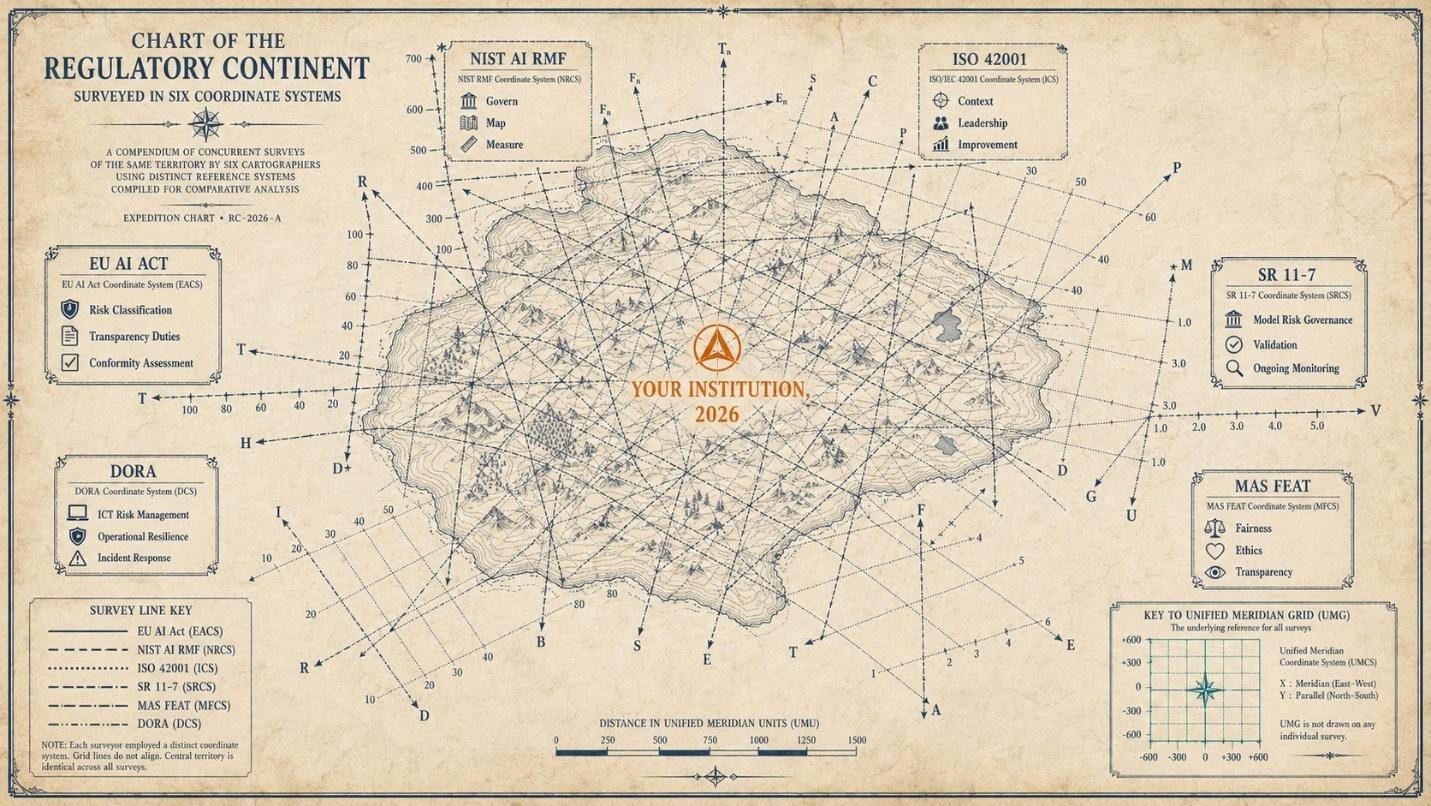

Across jurisdictions, oversight now runs through sector regulators in the United States, the EU AI Act, and global standards such as ISO/IEC 42001 and NIST AI RMF. Each uses different language. All converge on a single requirement: evidence.

For a bank, asset manager, broker-dealer, or insurer, the regulatory map of AI now looks like a continent surveyed by half a dozen cartographers, each working from a different reference point. The terrain is the same, the same models making the same decisions about the same customers, but the rules drawn over it differ in vocabulary, scope, and evidentiary standard. The decision facing a CISO or compliance officer is not which framework to comply with. The decision is which single operational program produces evidence acceptable to all of them, applied to AI systems that no longer behave like the deterministic software the existing compliance stack was designed to govern.

Financial institutions are not failing AI compliance because they lack policies. They are failing because their systems cannot produce evidence at the moment regulators now inspect. The constraint is the gap between what those frameworks require as evidence of agent behaviour and what existing GRC infrastructure can actually produce. Closing that gap is not a documentation problem. It is an instrumentation problem, and it is solved at runtime.

What financial services regulators actually want from your AI agents

Read past the cover page of any of the current frameworks and a single word recurs: evidence. EU AI Act Article 12 mandates automatic event recording for high-risk systems. Article 13 requires that the system be designed for traceability and that deployers receive instructions sufficient to interpret and use the output. Article 14 sets out human oversight obligations that include the ability to intervene, override, and reconstruct. NIST AI RMF specifies measurable, traceable risk controls. ISO/IEC 42001 specifies management system records and corrective action audit trails. The March 2026 White House federal AI policy guidance expects the SEC and prudential agencies to apply existing examination doctrine, which already runs on documentary evidence.

Three questions sit beneath all of this, and regulators want each answered with proof, not policy.

First, who or what was authorised to take this action? When an agent retrieves a customer record, reprices a policy, or escalates a fraud flag, the institution must show that the action was performed by a specific identifiable system instance, operating within an authorised scope, against an authenticated principal. Reusing a service account credential across an agent fleet, which remains common, fails this question on inspection.

Second, what was the system's reasoning state at the moment of decision? For a credit decisioning agent that combined three tools, retrieved one external dataset, and revised its plan twice, a tabular log of input-output pairs is not a sufficient record. The plan, the tool calls, the policy checks performed, and the policy checks skipped all need to be reconstructible.

Third, how can the institution verify, after the fact, that the recorded answer to the first two questions has not been altered? Logs in a typical database can be modified by operators with sufficient access. EU AI Act Article 72 post-market monitoring obligations imply integrity. ISO/IEC 42001 management reviews expect authentic records. SR 11-7 audit work has always assumed integrity of artefacts. Most current GRC stacks do not produce cryptographic proof of integrity. They produce records that are usually correct, which is a different thing.

Most coverage frames AI compliance for financial services as a documentation challenge. The framing is wrong. Regulators are not asking institutions to write better policies. They are asking institutions to produce records of agent decisions that are integrity-protected, reconstructible, and shareable with supervisors on request. The work is closer to evidence handling in a regulated industry than to policy authoring.

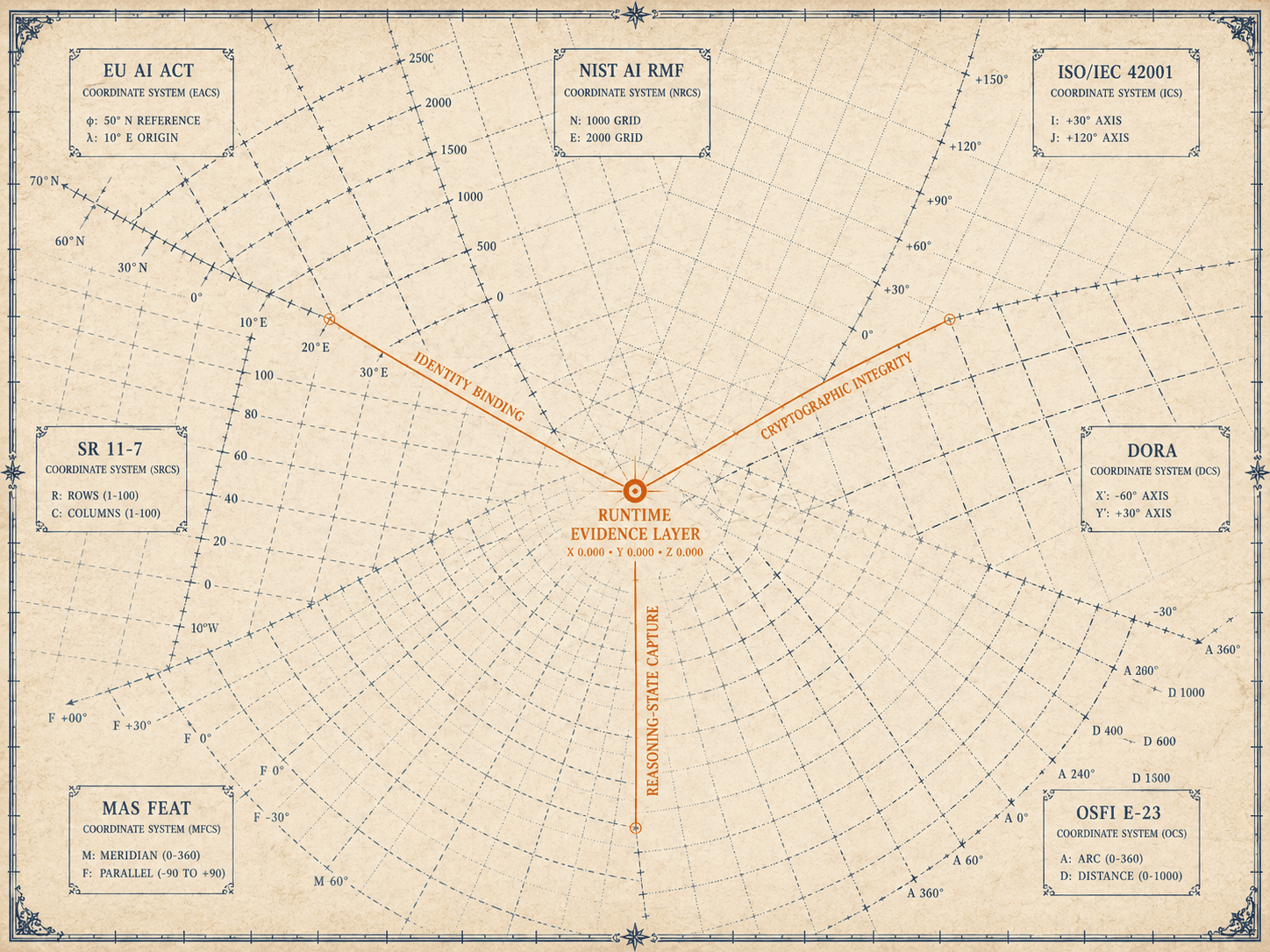

Within this system, Cryptographic Attestation ensures that each recorded session is sealed and independently verifiable. Each governance session produces a sealed, tamper-evident record of agent behaviour that can be independently verified. The signature represents proof of what happened at runtime, not a record constructed afterwards. Blocked actions are recorded alongside permitted ones, which matters when an examiner asks not only what the system did, but what it attempted to do.

Why 2026 compresses compliance timelines

Three dates frame the financial services compliance year. The 2 August 2026 application date for Annex III high-risk AI under the EU AI Act is the most operationally consequential, because two of the listed categories, creditworthiness assessment and risk pricing in life and health insurance, sit squarely inside the day-to-day business of regulated finance. The Digital Omnibus proposal, currently before the European Parliament and Council, may extend specific deadlines if harmonised standards are not ready, but supervisors have been clear that institutions should plan for August 2026 and treat any extension as contingency, not strategy.

The March 2026 federal AI policy guidance issued by the White House is the second date. Its content is non-binding, and its institutional signal matters more than its text. Federal AI policy in the United States will route through sector regulators that already supervise financial institutions, rather than through a new federal AI agency. For compliance teams, the form of AI oversight will look like the form of oversight they already operate under, with familiar examination patterns and familiar consequences for inadequate documentation. The policy guidance's preemption proposals, if enacted, would not lift the substantive expectation. They will redirect it.

The third date is older and easier to forget. ISO/IEC 42001, the international standard for AI management systems, has been available since December 2023, which means certification audits in 2026 are no longer concept demonstrations. They are happening, they are being requested by enterprise customers as a condition of vendor selection, and the gap between an institution's stated AI governance and what an auditor can actually verify has become a commercial fact, not just a regulatory one.

Add the standing requirements: NIST AI RMF for federal contractors and a growing list of voluntary adopters; SR 11-7 and OCC supervisory expectations for US banks; EBA outsourcing guidelines for European institutions; MAS FEAT principles for Singapore-supervised firms; OSFI Guideline E-23 in Canada; DORA for EU operational resilience; FCA and SM&CR accountability obligations for UK firms, where AI-driven decisions may fall within the scope of senior manager responsibility under existing conduct rules depending on supervisory interpretation and enforcement context. Several overlapping authorities expect the same underlying capability: identity-bound, integrity-protected, replayable evidence of what AI systems did and why.

The institutions now entering 2026 examinations are not failing on policy. They are losing on a structural failure mode: treating publication of an AI governance policy as the act of operating one. Examiners do not make that substitution. The policy is an artefact. The program is what the policy can prove about live agent behaviour on a representative day in production.

Taken together, these timelines collapse the distance between policy readiness and evidentiary readiness. Institutions are no longer preparing for compliance. They are being tested on it.

Why the standard model risk playbook fails on agentic systems

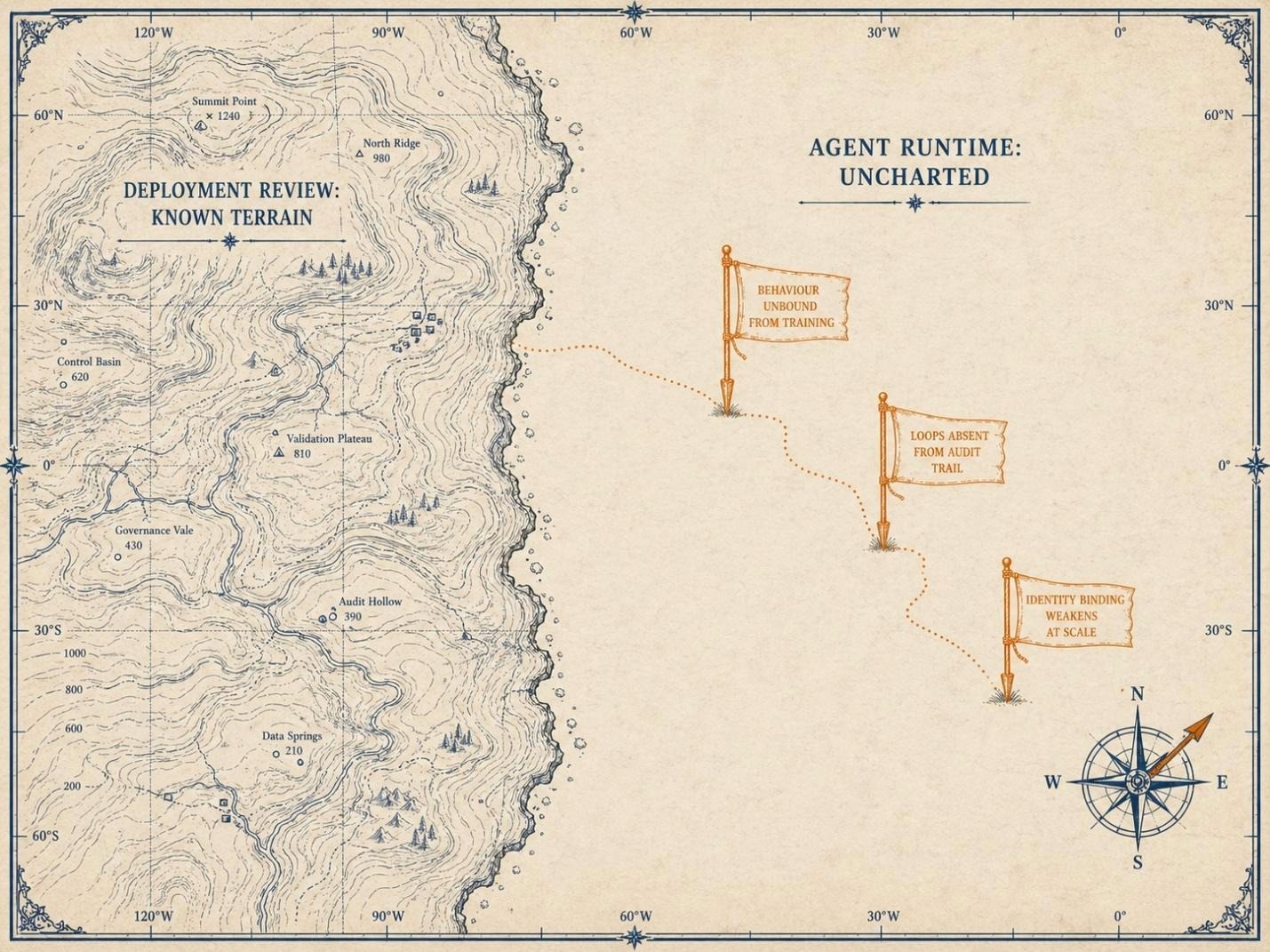

Model risk management as a discipline was built around static models. A scorecard, a default probability model, a stress engine. These artefacts are reviewable: their inputs are bounded; their behaviour is predictable enough that a model risk committee can validate the deployed version against the reviewed version and trust the comparison. The discipline has served financial services well for two decades. It does not survive contact with agentic AI.

Call this the model-agent gap: the gulf between what was approved at deployment review and what an agent actually does at runtime. The gap is the structural reason the SR 11-7 playbook produces false comfort when applied unchanged to agentic systems. Three failure points open it.

First, agent behaviour is not bounded by training distribution. Behaviour is shaped at runtime by tools, prompts, and goal configuration, not just training data. A model risk review at deployment time tells the institution very little about whether the agent will, six months later, be reading a complaint email containing instructions designed to redirect its behaviour towards an action the original review never considered.

Second, traditional ML audit trails do not capture agent loops. An agent that planned, called external tools, revised its plan, called more tools, and acted across multiple steps cannot be reconstructed from input-output pairs. Examiners reviewing a 2027 incident will ask for the reasoning chain, the tool invocations, the policies that were checked, and the policies that were skipped. If the institution can produce only the action and the outcome, the case is lost before the examiner has finished asking the question. Agentic systems do not execute a single model decision; they orchestrate sequences of tool calls, external data retrieval, and policy checks. The unit of compliance is no longer the model output but the full execution trace.

Third, identity binding is structurally weaker for agents than for humans. A human operator carries a credential, a session, and an entitlement matrix tied to a role and reviewed annually. An agent calling APIs as the user it serves inherits permissions designed for human pace and judgment, then uses them at machine pace without the contextual hesitation a person would apply. A control surface that worked for a human in the loop does not work when the loop runs at agent speed.

Each of these three failure points is closed by the same architectural response: enforcement at the action level, not review at the deployment level. Within the enforcement layer, the Authorize phase evaluates identity, scope, and policy at each action. Policies, expressed as OPA/Rego stateless permission checks, evaluate what agent is acting, under what principal, against what authorised scope, before the action executes. A credit decisioning agent calling an external data enrichment endpoint receives a policy decision at that exact call, not a blanket permission carried forward from a deployment-time approval. Behavioral Rules detect the multi-step patterns that no single-operation check would catch.

The evidence layer your existing GRC stack cannot produce

This is the gap OpenBox is built to close. OpenBox operates as a runtime governance layer embedded directly in the execution path of AI systems. It does not sit alongside existing infrastructure as a reporting or monitoring tool. It sits inside the decision loop, evaluating and enforcing policy at the point an action is taken, while producing verifiable records of that action.

The system combines three functions that existing stacks separate:

• Enforcement: policy decisions evaluated at each agent action

• Evidence capture: full reasoning-state and execution trace recorded at runtime

• Verification: cryptographic sealing of records to ensure integrity

These functions operate continuously across the agent session, not post-hoc.

The Trust Lifecycle is OpenBox’s runtime governance system. It is not a reporting framework; it is an enforcement system that turns regulatory requirements into executable controls.

GRC platforms remain useful for policy management, control mapping, and audit coordination. They were not designed to capture agent runtime behaviour, and they do not produce the evidence regulators are now expecting. The control GRC stacks offer is documentary. The control regulators are asking for is enforcement at the point of action.

The shift required is from observability, recording what happened, to runtime enforcement, deciding at the point of action whether the action should happen at all. The distinction is the difference between a flight data recorder and a pre-flight safety check. A recorder captures what happened after an incident. A safety check prevents the incident from occurring. Examiners increasingly want both, and they want to see how the two relate.

This is not the first time financial services compliance has made this architectural shift. The Basel III liquidity coverage ratio required banks to maintain and evidence a daily measurable liquid asset position. Compliance was not achieved by writing a policy about liquidity management. Compliance was achieved by maintaining an always-current, auditable position that could be produced on demand. Regulators did not accept a policy statement about liquidity as a substitute for the measurement itself. The same architecture is now being applied to AI governance.

This reframes the definition of compliance:

Compliance is not the policy you wrote about your AI. It is the evidence position you can produce about AI behaviour on any day in the past quarter. |

The Trust Lifecycle is OpenBox’s five-phase runtime governance system:

• Assess: builds a risk profile for each agent

• Authorize: enforces identity, scope, and policy at each action

• Monitor: records all governance events in real time

• Verify: checks whether actions align with the agent’s authorised purpose

• Adapt: updates policy based on observed behaviour

Each session produces a cryptographically sealed record, including both permitted and blocked actions.

Regulators are quietly converging on a single evidentiary substrate. EU AI Act post-market monitoring, US safe-harbor provisions aligned with the March 2026 White House AI policy guidance, ISO/IEC 42001 audit trails, OCC supervisory expectations, and DORA operational resilience requirements can all be satisfied by the same underlying record, provided the record carries three properties: identity binding, cryptographic integrity, and reasoning-state capture. Institutions that instrument this layer once, correctly, are positioned to map the same record onto whatever the next regime asks. Institutions that build a separate pipeline per framework pay for the same capability several times and produce inconsistent versions of the truth.

All major regulatory regimes converge on the same evidentiary requirements. The table below shows how a single runtime record satisfies each.

Framework | Evidence type required | Integrity standard | Producible from runtime governance? |

EU AI Act (Art. 12, 13, 14, 72) | Automatic event records, traceability, post-market monitoring | Authentic, tamper-resistant | Yes |

ISO/IEC 42001 | Management system audit trail, corrective action records | Authentic, retained | Yes |

NIST AI RMF 1.0 | Measurable, traceable risk controls; measurement results | Documented, defensible | Yes |

SR 11-7 / OCC model risk | Validation evidence, ongoing monitoring, change control | Independent, verifiable | Yes |

DORA (EU) | ICT incident records, third-party register, resilience tests | Auditable, reportable | Yes |

MAS FEAT, OSFI E-23 | Fairness, ethics, accountability, transparency records | Examinable | Yes |

The implication is operational: one evidence architecture can satisfy multiple frameworks without duplicating compliance pipelines.

Behavioral Rules add a layer most GRC stacks cannot reach: detection of agent goal drift before it becomes a material event. An agent that begins a session helping a customer understand mortgage options and ends it advising on portfolio reallocation has drifted out of authorised scope. Under the EU AI Act's foreseeable misuse provisions, and understanding model risk doctrine, that drift is a compliance signal, not just an operational quirk. Catching it during the session, recording the detection in the session record, and routing the session to human review is the action that turns drift from an incident into an artefact.

FOR THE MODEL RISK OFFICER READING THIS The discipline you bring to model validation is the right starting point. The change is that the artefact under review is no longer a frozen model; it is a runtime trace. Equip your validation team to read signed session records the same way they read coefficient tables. The validation work is not new. The medium of the evidence is. |

A 90-day path through the regulatory landscape

The instinct, in front of a fragmented regulatory map, is to commission a multi-quarter program managed by committee. The institutions landing well in 2026 examinations did not do that. They did three things, in order.

Days 1 to 30: inventory and classify. List every AI system in production, every agentic workflow under development, and every third-party AI feature embedded in vendor software the institution uses. Classify each by EU AI Act risk tier, by sector-specific impact, and by whether the system makes decisions the institution would need to defend before a tribunal or examiner. Most institutions discover their inventory is roughly twice as long as the model risk register suggests, because agentic features inside SaaS tools were never registered and copilots inside back-office software were never reviewed. One global custodian completing this step found 34 agent workflows in production that had never passed a model risk committee, 14 of which touched customer account data on every invocation with no reasoning-state audit trail. The inventory alone became the compliance officer's basis for moving the governance program from optional to urgent.

Days 31 to 60: close the evidence layer. For each high-impact system, instrument the runtime path to produce attributed, integrity-protected records of every agent action and the reasoning state at the moment of action. SDK-level integration matters more than platform selection. The integration requirement is simple: the governance layer must sit directly in the agent’s action path without requiring architectural changes. If that condition is not met, it will not survive change-control constraints in regulated environments. That property, no architectural changes, is the only integration model that fits inside a regulated institution's change-control process on a 30-day clock. In practice, this often exposes hidden agent actions such as silent external API calls or undocumented tool chains that were never captured in model risk documentation.

Days 61 to 90: prove it on a real audit scenario. Pick one regime. The EU AI Act is usually the right choice because its evidentiary bar is the most demanding. Run a tabletop exercise: a supervisor asks for the full reasoning chain of one specific agent decision from the past quarter, with proof of integrity. Time the institution from request to delivered evidence. Anything over four hours is a structural problem, not a capacity one. A four-hour answer demonstrates the institution can satisfy multiple regimes from the same session record. A regional bank completed this step and used the attested session record to close a planned six-week examination inquiry in a single meeting: the examiner verified the integrity of three flagged sessions and closed the matter the same day.

Window | Deliverable | Owner | Pass test |

Days 1-30 | Complete AI system inventory across in-house, third-party, and embedded; risk-tier classification per Annex III and sector taxonomy | CISO and Chief Compliance Officer, joint | Inventory exceeds existing model risk register; gaps documented |

Days 31-60 | Runtime governance instrumented across high-impact systems; attested session records produced via single SDK | Head of AI Engineering, supported by GRC | Per-session signed records produced for every high-impact agent action; sample audit pack reviewed by internal audit |

Days 61-90 | Tabletop audit exercise against EU AI Act evidentiary bar; documented reconstruction time | Internal Audit, with Compliance and Engineering | Reasoning chain delivered with integrity proof in under four hours |

The 90-day window is not the only viable path. The window is the path that has produced supervisory comfort during actual examinations this year. Compressing it has consistently failed at the inventory step, because institutions skipped systems they did not yet know about. Extending it has lost momentum and ended in partial coverage that satisfied no regime fully. The institution that emerges from this window with a single integrated evidence architecture aligned with EU AI Act, NIST AI RMF, ISO/IEC 42001, sectoral expectations, and the next regime that has not yet been written is not the one that paid the most for AI compliance in 2026. It is the one that built the right capability once and instrumented it correctly.

AI compliance in 2026 is no longer a policy problem. It is an evidence architecture problem. Institutions that instrument runtime governance once satisfy multiple regimes from a single record. Those that do not fragment compliance and fail to produce consistent proof under examination.

Key terms

Term | Definition |

Trust Lifecycle | The Trust Lifecycle is the operational model through which the system executes: Assess, Authorize, Monitor, Verify, and Adapt. |

Cryptographic Attestation | Production of integrity-protected, cryptographically signed records of agent behaviour. Per-session records are sealed such that post-hoc modification is detectable. Blocked actions are attested alongside permitted ones. |

Runtime governance | Enforcement of identity, authorisation, and policy at the point an action is executed, before the action takes effect. The functional opposite of post-hoc observability. |

Guardrails | Hard constraints on agent actions. Specific guardrail types are detailed in the OpenBox guardrails documentation |

Behavioral Rules | Stateful multi-step pattern detection rules that track action sequences, frequencies, and combinations across a session to identify goal drift or policy violations no single-operation check would catch. |

Trust Score | The Trust Score is derived from three components: Risk Profile Score (40%), Behavioral compliance (35%), and Alignment with declared goals (25%). |

Model-agent gap | The structural gap between what was approved at deployment review and what an agent actually does at runtime, given runtime tool selection, prompt context, and goal-shaping inputs that did not exist at review time. |

Annex III (EU AI Act) | The list of AI use cases classified as high-risk. For financial services, the most operationally relevant entries are creditworthiness assessment and risk pricing in life and health insurance. |

Foreseeable misuse | A concept in the EU AI Act requiring providers and deployers to anticipate and address reasonably foreseeable adverse uses of high-risk systems, including misuse arising from agent goal drift or adversarial input in user-provided content. |